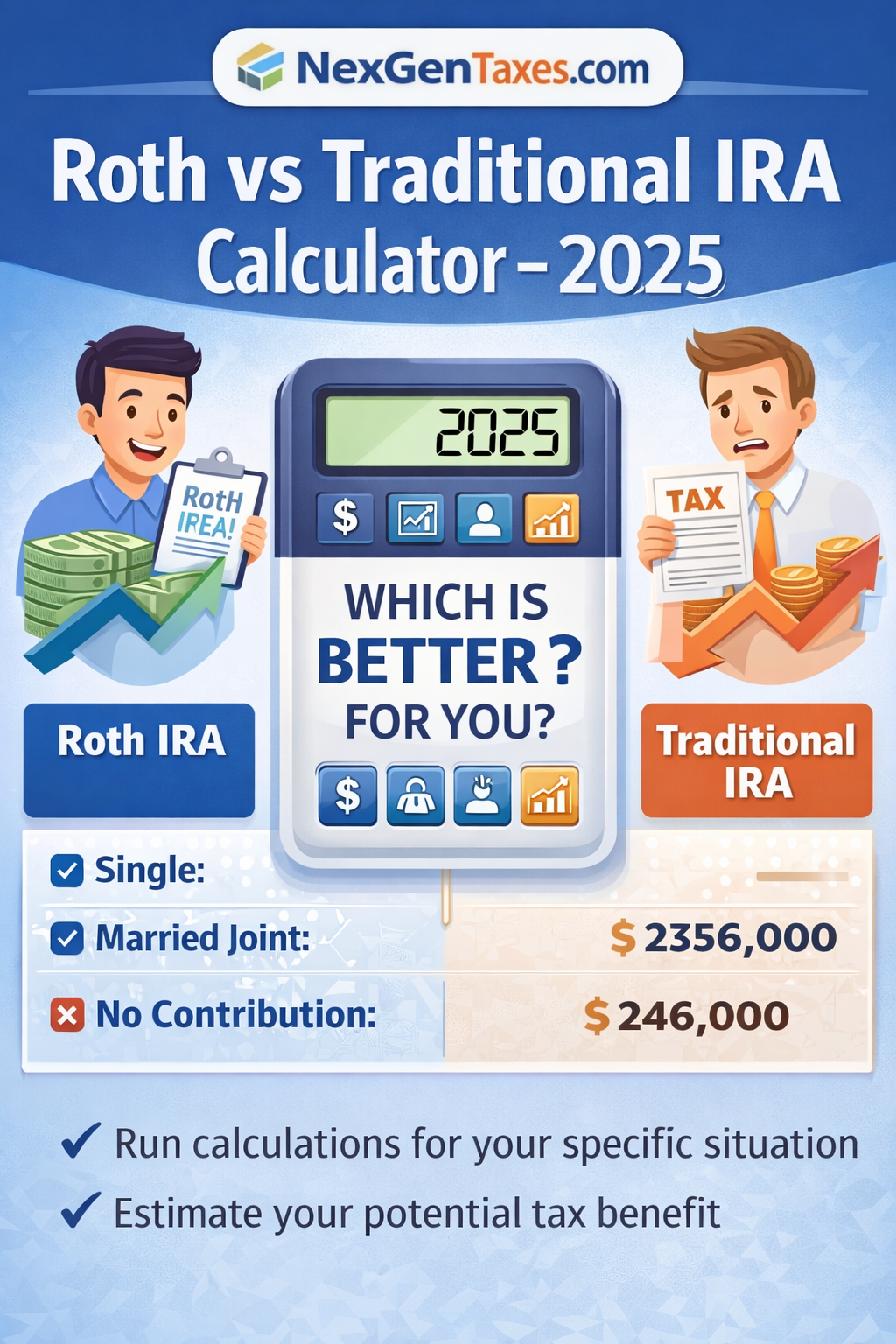

What's the difference between Roth and Traditional IRA?

A Traditional IRA offers tax-deductible contributions now, with tax-deferred growth, but withdrawals in retirement are taxed as ordinary income. A Roth IRA uses after-tax contributions (no immediate tax break), but the account grows tax-free and qualified withdrawals in retirement are completely tax-free.

The key difference is when you pay taxes: now (Roth) or later (Traditional). Think of it as choosing between a tax break today versus tax-free income in retirement. Use our Tax Bracket Calculator to understand your current bracket.